On this page

AI infrastructure tools adoption statistics for 2026 show that 72% of enterprises now have at least one AI workload in production, AI infrastructure spending has reached an estimated $101 billion globally, and the MLOps market stands at $3.4 billion — yet over 80% of organizations report no tangible bottom-line impact from their AI investments. These figures define the current state: massive investment, rapid deployment, but a persistent gap between adoption and realized returns.

Finding reliable AI infrastructure adoption statistics is harder than it should be. Market sizing figures from major research firms can vary by a factor of three for the same segment, enterprise adoption surveys arrive at wildly different percentages depending on how "AI use" is defined, and vendor-published reports are invariably optimistic. This article cuts through that noise.

What follows is a curated, sourced collection of AI infrastructure tools adoption statistics for 2026 — organized by category, with methodology notes where figures conflict, and with context that helps you interpret the data rather than simply collect it. Whether you're benchmarking your own deployment or building a business case, these AI infrastructure tools adoption statistics provide the ground-level data you need.

Key Takeaways

- The AI infrastructure market reached an estimated $101 billion in 2026 (Mordor Intelligence), with hardware — primarily GPUs — accounting for 54% of that spend.

- 72% of enterprises have at least one AI workload in production as of Q1 2026, up from 55% in 2024 and just 20% in 2020 (McKinsey Global AI Survey).

- 82% of enterprises are not ready for the infrastructure demands of their stated AI ambitions (Nutanix Enterprise Cloud Index 2026).

- The MLOps market — covering the platforms and tools that operationalize AI — reached $3.4 billion in 2026 and is projected to grow to $25.93 billion by 2034 (Fortune Business Insights).

- Inference now drives 60–70% of total AI compute demand at major hyperscalers, up from ~40% in 2024, reshaping which infrastructure tools enterprises actually need.

- Over 80% of organizations report no tangible EBIT impact from generative AI adoption despite significant investment — a key tension between infrastructure spend and realized returns.

AI Infrastructure Adoption Statistics: Quick Reference

| Metric | Statistic | Source |

|---|---|---|

| AI infrastructure market size (2026) | $101.17 billion | Mordor Intelligence |

| Enterprise AI workloads in production | 72% of enterprises | McKinsey |

| Enterprises not ready for AI demands | 82% | Nutanix |

| MLOps market size (2026) | $3.4 billion | Fortune Business Insights |

| LLMOps market size (2026) | $7.14 billion | Research and Markets |

| GPU-as-a-Service market (2026) | $7.38 billion | Mordor Intelligence |

| GPU market share (NVIDIA) | 78–80% in AI training | Medhacloud |

| Inference share of AI compute | 60–70% | AceCloud |

| Enterprises with mature AI adoption | 28% | Medhacloud |

| AI agent adoption (enterprises) | 51% in production | Gartner/Ringly |

| AI projects stuck in pilot phase | ~50% | Reinventing AI |

| Enterprises reporting productivity gains | 66% | Deloitte |

| Enterprises with no EBIT impact | 80%+ | CXOVoice |

| Top industry AI adoption | Technology (94%) | Second Talent |

| North America AI infrastructure share | 39.56% (2025 revenue) | Mordor Intelligence |

Table of Contents

- What Are AI Infrastructure Tools?

- AI Infrastructure Adoption Statistics: Quick Reference

- AI Infrastructure Market Size and Spending Statistics (2026)

- Enterprise AI Infrastructure Adoption Statistics and Rates

- MLOps and LLMOps Platform Adoption Statistics

- AI Hardware and GPU Compute Statistics

- Cloud vs. On-Premises vs. Hybrid AI Infrastructure Trends

- AI Infrastructure Adoption by Industry

- Barriers to AI Infrastructure Adoption

- AI Infrastructure ROI and Productivity Statistics

- Geographic Distribution of AI Infrastructure Investment

- AI Infrastructure Outlook: 2027–2030 Projections

- Frequently Asked Questions

What Are AI Infrastructure Tools?

AI infrastructure tools are the hardware, software, and managed services that enable organizations to build, train, deploy, and monitor AI and machine learning models at scale. The category includes compute resources (GPUs, TPUs, custom accelerators), cloud AI platforms (AWS SageMaker, Google Vertex AI, Azure ML), MLOps and LLMOps platforms for managing model lifecycles, data pipelines, feature stores, and observability tools for tracking model performance in production environments.

The category is distinct from AI applications (the products built on top of infrastructure) and from general cloud infrastructure. When researchers report on "AI infrastructure," they typically include:

- Compute hardware: GPUs, NPUs, AI-optimized servers

- Cloud AI services: managed training and inference platforms

- MLOps platforms: tools for experiment tracking, model registries, pipeline orchestration, and model monitoring

- LLMOps tools: infrastructure specifically built for large language model deployment and management

- AI data infrastructure: feature stores, data lakehouse architectures, vector databases

Note: Market sizing figures in this article vary significantly depending on which of these layers each research firm includes. When figures conflict, we explain why.

AI Infrastructure Market Size and Spending Statistics (2026)

Market sizing for AI infrastructure varies widely across research firms, primarily because each uses a different scope. Here are the key figures:

Headline figures (2026 estimates):

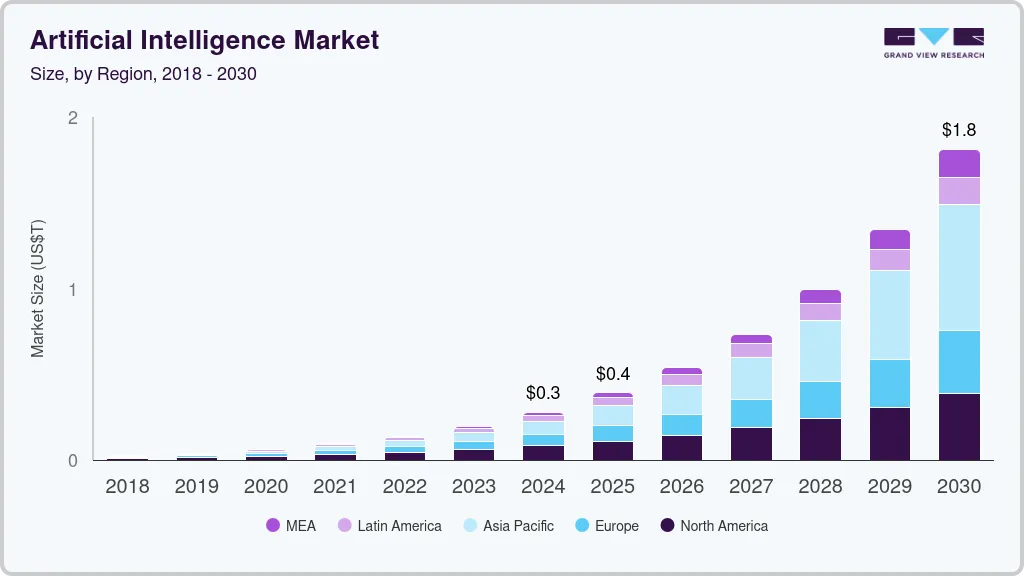

- $101.17 billion — Mordor Intelligence, projected to reach $202.48B by 2031 at a 14.89% CAGR. This figure covers hardware, software, and services in the AI infrastructure stack.

- $98 billion — IDC estimate for global AI infrastructure spending in 2026, primarily covering AI chips, servers, and networking hardware.

- $75.40 billion — Fortune Business Insights, growing to $497.98B by 2034. Uses a narrower scope focused on hardware and compute platforms.

- $31.12 billion — Gartner (via Second Talent), specifically for AI platforms, data science, and ML tools (a software-only subset).

Why the figures differ: Mordor and IDC include hardware, networking, and cloud services. Gartner's $31B figure counts only the software tooling layer. Fortune Business Insights uses a narrower hardware-forward definition. None of these figures is "wrong" — they measure different things.

Key segment figures:

- MLOps market: $3.4 billion in 2026, projected $25.93 billion by 2034 (28.90% CAGR)

- LLMOps market: $7.14 billion in 2026, growing to $15.59 billion by 2030 at 21.3% CAGR

- GPU-as-a-Service: $7.38 billion in 2026, projected $26.09 billion by 2031 (28.73% CAGR)

Overall AI spending context:

- AI data center capex is expected to reach $400–$450 billion globally in 2026, with $250–$300 billion in chips alone (Deloitte)

- AI infrastructure spending is on track to reach $758 billion by 2029 (IDC)

Enterprise AI Infrastructure Adoption Statistics and Rates

Production workload deployment:

- 72% of enterprises have at least one AI workload in production as of Q1 2026, up from 55% in 2024 and 20% in 2020 (McKinsey Global AI Survey)

- 78% of organizations use AI in at least one business function — this was McKinsey's 2024 baseline; by 2025, McKinsey's own updated survey reported the figure had risen to 88%

- 76%+ of respondents from large enterprises (1,000+ employees) report active AI usage; only 2% say they don't use AI at all (CXOVoice)

Maturity and scale:

- 28% of enterprises describe their AI adoption as "mature" — meaning 72% are still in early or growth stages (Medhacloud)

- 87% of large enterprises have implemented AI solutions; large enterprises account for 54.89% of MLOps market share globally in 2026 (Fortune Business Insights)

- 51% of enterprises have AI agents in production; Gartner projects 40% of enterprise applications will integrate AI agents by end of 2026 (Ringly)

The readiness gap:

- 82% of enterprises report they are not ready for AI infrastructure demands despite active investment (Nutanix Enterprise Cloud Index 2026)

- 45.6% of organizations don't know their own AI-adoption rate — a significant governance and visibility gap (Larridin State of Enterprise AI)

- ~50% of agentic AI projects remain stuck in pilot stages and have not reached production (Reinventing AI)

Investment levels:

- 59% of companies invest over $1 million annually in AI technology (Medhacloud)

- Enterprise AI spending averages $1,240 per employee annually at companies with 500+ employees

The adoption data reveals an important nuance: while headline AI infrastructure tools adoption statistics show high rates, most organizations are still in early deployment phases, and a large readiness gap exists between what enterprises are spending and what their infrastructure can actually support.

MLOps and LLMOps Platform Adoption Statistics

MLOps (Machine Learning Operations) and LLMOps (Large Language Model Operations) are the tooling categories that bridge AI model development and production deployment. Their adoption tells a more specific story about infrastructure tool uptake than general AI adoption surveys.

Market growth:

- MLOps market: $3.4 billion in 2026 → $25.93 billion by 2034, at 28.90% CAGR (Fortune Business Insights)

- LLMOps market: $7.14 billion in 2026 → $15.59 billion by 2030, at 21.3% CAGR (Research and Markets)

- Cloud segment accounts for 54.89% of MLOps market in 2026; the hybrid segment is growing at the fastest CAGR (Fortune Business Insights)

Tool landscape in 2026:

Research from LakeFS and AIMultiple identifies the dominant tools by category:

| Category | Leading Tools |

|---|---|

| Experiment tracking | MLflow, Weights & Biases |

| Pipeline orchestration | Kubeflow, Apache Airflow, Prefect, ZenML |

| Model registry | MLflow Model Registry, Hugging Face Hub |

| Feature stores | Feast, Tecton, Hopsworks |

| Model monitoring | Evidently AI, Arize AI, Fiddler AI |

| Full ML platforms | AWS SageMaker, Google Vertex AI, Azure ML, Databricks |

Adoption outcomes:

- Companies implementing MLOps properly report 40% cost reductions in ML lifecycle management and 97% improvements in model performance (AIMultiple)

- 63% of organizations use open-source AI tools; 76% expect to increase open-source AI usage, indicating continued growth for tools like MLflow and Prefect (AIMultiple)

Enterprise pattern: The dominant approach in 2026 combines a managed cloud platform (SageMaker, Vertex AI, or Azure ML) with open-source tools for portability and cost control — rather than a single-vendor stack. This reflects both cost optimization pressures and vendor lock-in concerns.

AI Hardware and GPU Compute Statistics

Hardware dominates AI infrastructure investment. The following statistics capture the current state of AI compute.

Market share and spending:

- Hardware accounts for 54% of AI infrastructure market share in 2026; GPUs retain 88.82% of revenue within the hardware segment (Mordor Intelligence)

- NVIDIA holds approximately 78–80% market share in AI training GPUs; AMD at ~12%; Intel and custom silicon at ~10% (Medhacloud)

- AI data center capex expected to reach $400–$450 billion globally in 2026; chips alone represent $250–$300 billion of that figure (Deloitte)

Growth rates:

- Worldwide server market spending grew 97.3% year-over-year in Q2 2025 (AceCloud)

- AI server shipments grew approximately 28% year-over-year in 2025 (TrendForce, via AceCloud)

- GPU spending jumped from $30 billion in 2022 to $50 billion in 2023 — a 67% year-over-year increase (PatentPC)

The inference shift — a structural change in AI infrastructure:

- Inference now accounts for 60–70% of total AI compute demand across major hyperscalers, up from approximately 40% in 2024 (AceCloud)

- AI workloads account for 24% of all public cloud compute spend (Medhacloud)

This shift from training-heavy to inference-heavy compute has practical implications for infrastructure tool selection. Training workloads demand large GPU clusters over short bursts; inference workloads require always-on, low-latency infrastructure optimized for throughput. Organizations building for the inference era need different tooling than those focused on model development.

Cloud vs. On-Premises vs. Hybrid AI Infrastructure Trends

Current state:

- 68% of enterprises have adopted cloud-based AI services; 68% of IT leaders report AI integration in cloud infrastructure (Medhacloud)

- Public cloud holds 67.19% of GPU-as-a-Service revenue in 2025; the hybrid/multi-cloud segment is advancing at a 29.36% CAGR (Mordor Intelligence)

The hybrid shift:

- By 2028, 75% of enterprise AI workloads will operate on tailor-made hybrid infrastructures, according to IDC forecasts (Tech-Insider.org)

- The hybrid segment of MLOps platforms is growing at the fastest CAGR of any deployment model in 2026 (Fortune Business Insights)

Cost context:

One underreported factor driving cloud AI adoption is cost deflation. The cost of querying a GPT-3.5-level model dropped from $20 per million tokens in November 2022 to $0.07 per million tokens by October 2024 — a 280-fold reduction (CXOVoice). That decrease has made cloud-based AI infrastructure economically viable for organizations that would have found it prohibitive just two years prior.

AI Infrastructure Adoption by Industry

Industry-level adoption varies significantly. The table below summarizes key figures from 2026 research:

| Industry | Adoption Rate / Key Stat | Source |

|---|---|---|

| Technology | 94% — highest of any sector | Second Talent |

| Financial Services (BFSI) | 85% use AI in at least one area; 19.60% AI infrastructure market share | Medhacloud |

| Healthcare | 62% adoption; fastest-growing sector at 19.10% CAGR | CXOVoice |

| Retail | 53% use AI for forecasting, personalization, or inventory | Medhacloud |

| Manufacturing | 48% YoY AI spending growth; focus on predictive maintenance | Medhacloud |

| Telecom | 48% agentic AI adoption — highest of any industry | CXOVoice |

| Education | 34% — lowest adoption; constrained by budget and regulation | Medhacloud |

Financial services leads AI infrastructure investment in absolute terms, spending $3,200 per employee annually on AI — 2.6x the cross-industry average (Medhacloud). Healthcare's fast CAGR reflects both clinical decision support applications and mounting regulatory requirements that are accelerating investment.

SMB vs. enterprise divergence:

- 74% of SMBs use AI indirectly through embedded features in existing tools — not via dedicated AI infrastructure (Medhacloud)

- Only 12% of SMBs have a dedicated AI strategy

- 67% of MSPs now offer AI-related services, making managed service providers an increasingly important distribution channel for AI infrastructure tools (Medhacloud)

Barriers to AI Infrastructure Adoption

High-level adoption rates obscure the significant challenges organizations face in building functional AI infrastructure. Research from 2025–2026 consistently surfaces the same obstacles:

Skills and talent:

- 46% of tech leaders cite AI skill gaps as a major obstacle (IBM, via CXOVoice)

- Up to 90% of organizations will face IT talent shortages; estimated $5.5 trillion in projected losses by 2026 from skills gaps (CXOVoice)

Integration with legacy systems:

- 95% of IT leaders report integration issues that prevent AI implementation (Larridin)

- 60% of AI leaders cite legacy integration as the primary challenge for agentic AI deployment (Larridin)

Data quality:

- 64% cite data quality as their top challenge; 77% rate their own data quality as "average or worse" (Deloitte State of AI 2026)

- 41% of SMBs cite data quality as a specific barrier to AI adoption

Governance and visibility:

- 45.6% of organizations don't know their own AI-adoption rate (Larridin)

- Only 21% have mature AI governance models

- 36% lack any formal plan for supervising AI agents in production (Larridin)

Shadow AI:

- 87% of IT executives believe unauthorized AI tools create business risk (Codewave)

- 79% encounter AI implemented by non-IT employees — usage that bypasses infrastructure standards and security controls

The pilot-to-production gap:

- Approximately 50% of agentic AI projects remain stuck in pilot stages (Reinventing AI)

- Gartner forecasts that 40%+ of agentic AI initiatives will be canceled by end of 2027, primarily due to infrastructure complexity and unclear ROI (CXOVoice)

This last point is worth dwelling on: the high cancellation rate for agentic AI projects is not primarily a model quality problem — it's an infrastructure and integration problem. Organizations that can't reliably connect AI systems to the data and APIs they need cannot move beyond proof-of-concept.

AI Infrastructure ROI and Productivity Statistics

ROI data for AI infrastructure is mixed in 2026. The gap between adoption rates and realized returns is one of the defining features of the current market.

Positive outcomes:

- Median time to ROI dropped from 24 months in 2024 to 14 months in 2026 (Medhacloud)

- 66% of organizations report productivity or efficiency gains from enterprise AI adoption (Deloitte State of AI 2026)

- Average productivity value of generative AI tools: $7,800 per knowledge worker per year (Accenture, via Netguru)

- 38% of knowledge workers use generative AI tools daily, up from 11% in 2024 (CXOVoice)

- Companies implementing proper MLOps tooling report 40% reductions in ML lifecycle management costs (AIMultiple)

The ROI gap:

- Over 80% of organizations report no tangible EBIT impact from generative AI adoption despite investment (CXOVoice)

- Only 20% of enterprises report already growing revenue through AI (Deloitte State of AI 2026)

- Only 29% of companies are seeing significant returns from AI investment (McKinsey)

The divergence between productivity gains (widely reported) and EBIT impact (rarely observed) reflects the early-stage nature of enterprise AI deployment. Most value so far has been captured in efficiency improvements at the team level rather than as margin expansion at the organization level. Analysts expect this to shift as organizations mature from adoption to optimization — but the data currently shows that expectation has not yet materialized at scale.

Geographic Distribution of AI Infrastructure Investment

North America:

- The United States represents 38% of global AI investment (Mordor Intelligence)

- North America held 39.56% of 2025 AI infrastructure revenue and 42.36% of GPU-as-a-Service market share

China:

- China represents 26% of global AI investment (IDC)

- China is expected to grow at the fastest CAGR of 41.5% in AI infrastructure spending through 2029 (IDC)

- China accounted for 69.7% of all AI patent grants in 2023 — a leading indicator of where future AI infrastructure innovation may originate (CXOVoice)

Asia-Pacific (ex-China):

- Asia-Pacific holds 22% share in 2026 and is expected to grow at a 16.44% CAGR through 2031 (Mordor Intelligence)

- GPU-as-a-Service is growing fastest in Asia-Pacific at a 29.76% CAGR

Europe:

- The EU represents approximately 18% of global AI investment (Medhacloud)

- The US introduced 59 AI-related federal regulations in 2024 — more than double 2023's count — and European regulatory pressure via the EU AI Act is intensifying compliance requirements that affect infrastructure tool selection (CXOVoice)

AI Infrastructure Outlook: 2027–2030 Projections

Market sizing projections:

- AI infrastructure spending to reach $758 billion by 2029 (IDC)

- Global AI spending (broad definition, including applications) to reach $632 billion by 2028 (Medhacloud)

- AI projected to contribute $15.7 trillion to the global economy by 2030 (CXOVoice)

Infrastructure architecture trends:

- By 2028, 75% of enterprise AI workloads will run on hybrid infrastructure (IDC, via Tech-Insider.org)

- Over 75% of AI models will rely on specialized chips — GPUs, NPUs, TPUs, or custom accelerators — by 2026 (PatentPC)

Agentic AI and enterprise application integration:

- 33% of enterprise software will include agentic AI by 2028 (Gartner, via Ringly)

- This projection implies a significant infrastructure buildout: every agentic AI integration requires orchestration tooling, API connectivity, monitoring, and governance layers

The counterpoint:

Gartner's forecast that 40%+ of agentic AI initiatives will be canceled by end of 2027 (CXOVoice) is a notable check on the optimistic projections above. The organizations most likely to weather this consolidation are those that have invested in proper infrastructure tooling — MLOps platforms, observability, and integration layers. Those who bolted AI onto existing systems without architectural changes are most at risk.

Bottom line: The AI infrastructure market is large and growing. AI infrastructure tools adoption statistics through 2030 point to sustained investment — but the data also suggests that investment alone is not sufficient. The organizations seeing ROI are those that have built the operational infrastructure to manage AI reliably, not just those that have deployed it.

Frequently Asked Questions

How much is being spent on AI infrastructure in 2026?

Estimates range from $75 billion to over $100 billion for the AI infrastructure market in 2026, depending on scope. Mordor Intelligence estimates the market at $101.17 billion; IDC tracks approximately $98 billion in chips, servers, and networking hardware. AI data center capex alone is projected at $400–$450 billion globally in 2026 (Deloitte).

How Many Enterprises Have AI Workloads in Production (2026)?

72% of enterprises have at least one AI workload in production as of Q1 2026, up from 55% in 2024 and 20% in 2020, according to McKinsey's Global AI Survey. However, only 28% of enterprises describe their adoption as "mature" — most are still in early or growth stages.

What are enterprises' top AI spending priorities in 2026?

Based on current data, enterprises are prioritizing GPU compute (training and inference), cloud AI platforms (AWS SageMaker, Google Vertex AI, Azure ML), MLOps tooling for production model management, and LLMOps infrastructure for managing large language model deployments. AI data center construction and chip procurement represent the largest absolute spend categories.

Are large enterprises adopting AI faster than smaller ones?

Yes, significantly. Large enterprises (1,000+ employees) show 76%+ active AI usage rates. SMBs lag considerably: 74% use AI only through embedded features in existing software, and only 12% have a dedicated AI strategy. Enterprise AI spending averages $1,240 per employee annually at large companies — a level most SMBs cannot match.

How prepared are enterprises for AI infrastructure demands?

Not well. 82% of enterprises report they are not ready for their AI infrastructure demands (Nutanix Enterprise Cloud Index 2026). The primary gaps are skills (46% of tech leaders cite skill shortages), data quality (77% rate their own data as average or worse), and legacy system integration (95% of IT leaders report integration issues).

What is the state of AI agent adoption in enterprises?

51% of enterprises have AI agents in production as of 2026. However, approximately 50% of agentic AI projects remain stuck in pilot stages. Gartner forecasts that 40%+ of agentic AI initiatives will be canceled by end of 2027 due to infrastructure complexity and unclear ROI — suggesting that many organizations are not yet equipped to operationalize agentic AI reliably.

Are Enterprises Seeing ROI from AI Infrastructure?

Results are mixed. 66% of enterprises report productivity gains, and the median time to ROI has dropped from 24 months (2024) to 14 months (2026). However, over 80% report no tangible EBIT impact from generative AI adoption, and only 20% report growing revenue through AI. The gap between productivity-level improvements and P&L-level impact remains the defining challenge for enterprise AI programs in 2026.

What is the MLOps market size in 2026?

The global MLOps market is valued at approximately $3.4 billion in 2026, according to Fortune Business Insights, and is projected to grow to $25.93 billion by 2034 at a CAGR of 28.90%. The LLMOps market (focused specifically on large language model operationalization) is estimated separately at $7.14 billion in 2026.

What governance challenges exist around AI infrastructure?

Governance is a significant gap in 2026. Only 21% of organizations have mature AI governance models. 45.6% don't know their own AI-adoption rate. 36% lack any formal plan for supervising AI agents. 87% of IT executives believe unauthorized AI tools create business risk, and 79% report encountering AI deployed by non-IT employees. The US introduced 59 AI-related federal regulations in 2024 — more than double 2023's count — increasing compliance complexity.

Which Industry Has the Highest AI Infrastructure Adoption?

The technology sector leads all industries in AI infrastructure adoption, with a 94% adoption rate as of 2026. Financial services (BFSI) follows with 85% adoption and the highest absolute AI spending at $3,200 per employee annually. Telecommunications leads specifically in agentic AI adoption at 48%. Healthcare has the fastest growth trajectory, with a projected 19.10% CAGR driven by clinical decision support and medical imaging workloads.

How Does AI Adoption Differ Between Enterprises and SMBs?

Enterprise adoption significantly outpaces SMB adoption. Over 87% of large enterprises (1,000+ employees) have implemented AI solutions, while 74% of SMBs use AI only through embedded features in existing software tools rather than dedicated infrastructure. Only 12% of SMBs have a formal AI strategy. Enterprise AI spending averages $1,240 per employee annually at large organizations — a level most small businesses cannot match due to capital constraints.

What Percentage of AI Infrastructure Projects Get Canceled?

Approximately 50% of agentic AI projects remain stuck in pilot stages and never reach production as of 2026. Gartner forecasts that more than 40% of agentic AI initiatives will be canceled entirely by end of 2027, primarily due to infrastructure complexity, legacy system integration failures, and unclear ROI. The primary technical causes are data quality issues (cited by 64% of organizations) and legacy integration failures (cited by 95% of IT leaders).

How fast is the AI infrastructure market growing?

The AI infrastructure market is growing at a 14.89% CAGR according to Mordor Intelligence, with the market reaching $101.17 billion in 2026 and projected to hit $202.48 billion by 2031. Sub-segments are expanding faster: the MLOps market grows at 28.90% CAGR, the LLMOps market at 21.3% CAGR, and GPU-as-a-Service at 28.73% CAGR. China is the fastest-growing geography at a projected 41.5% CAGR through 2029, while North America holds the largest share at 39.56% of 2025 revenue.

All statistics in this article were sourced from publicly available research reports, industry surveys, and analyst publications. Market sizing figures from different research firms reflect different methodological scopes. Where figures conflict, we've noted the source and scope for each. Figures are current as of April 2026.

Related reading: AI tech stack statistics · AI Tools Overview · Industry Analysis

Get the weekly

One essay + 3 tools worth your attention, every Tuesday.

you@company.com